Solving Retention Bottlenecks for P2P Lending Apps in Indonesia

Southeast Asia’s massive underbanked population has proven to be a boon for numerous disruptive app-based mobile finance businesses. The disruption is surely massive on the consumer side of things but the B2B space has not remained untouched either. The growth of smartphone-based peer to peer lending/P2P lending apps in Indonesia is a testimony to that fact.

P2P lending apps primarily offer microfinancing to MSMEs but some of them are also providing quick loans for B2C consumers to help them cover their daily expenses.

In recent times, these apps have grown manifold by serving as marketplaces for lenders and borrowers to come together, transact and derive value at their respective ends. However, despite a growing number of customers and popularity, it is not easy for these mobile-first businesses to keep their customer base engaged and easily drive profits.

In this post, we will have a quick look into the P2P lending landscape in Indonesia along with the common retention bottlenecks that they encounter. In the end, we will look into the possibilities on how an insights-led approach can help entrepreneurs and marketers of these apps overcome these bottlenecks. So without further ado, let’s begin.

The P2P Lending Market in Indonesia

Indonesia is the undisputed leader in P2P lending in Asia. The country is home to more than 100 OJK registered lenders, trying to reach a whopping 47 million+ underbanked potential customers.

P2P lending apps are helping this massive base of potential customers become a part of this ecosystem by granting them quick loans without any hassle. The lenders on the other hand benefit by lending their funds for attractive rate of interest which is often much higher when weighed against other investment avenues.

In effect, P2P apps are helping the economy by allowing easy access to loans for small businesses and becoming an investment tool at the same time.

Additionally, P2P lending apps also provides a host of other value-added services to the lenders which motivates them to reinvest their earned commissions and stay invested. Lenders find these services valuable, making them stick to the apps and, in return, drive revenues for the P2P lending app.

While there are many apps out there in the market, only a few of them have significant transaction volume as an alternative lending destination. Asetku from Akulaku, Amartha Finance, Kredifazz from Finaccel, and Alami Sharia are prominent names that rule the P2P lending market with a substantial customer base and transaction volume.

Please note that adherence to the OJK regulatory framework is mandatory to launch and operate a P2P lending app or platform in Indonesia. It is not uncommon to see the government clean up shady P2P apps and companies from time to time in the country.

How do P2P Lending Apps Offer Value and Drive Retention?

Borrowers may install P2P lending apps for multiple reasons. While some might be looking to start a new business, others may simply want small amounts of financing to run their daily expenses on credit.

On the other hand, lenders can use these apps to earn higher interest rates by lending an amount. Additionally, they can also safeguard their earned income and simultaneously reinvest them into multiple investment options available within the app.

Whatever be their purpose, the overall app strategy of P2P apps revolves mainly around bridging lenders and loan applicants back to the app by providing value and developing habit loops over a period of time.

However, before a P2P app can reach that place, some important aspects must be set right.

These include onboarding reliable lenders, familiarizing investors with app features quickly, and engaging them on transaction updates using an omnichannel marketing approach.

| App activities that drive recurring usage by customers | News Feed providing latest information |

| Academy to train lenders/borrowers | |

| Check prices for commodities/gold | |

| Browsing app to find borrowers to reinvest accrued income | |

| App visit to fulfil the need of recurring loans (mostly B2C) | |

| Checking stream of incoming interest from borrowers | |

| Threshold – Manifests when the P2P business is moulded into an app | No Real time updates on events across multiple channels |

| Undiscovered app features/poor onboarding | |

| Time-consuming verification process to verify lenders | |

| Core Value Offerings – Reasons why lenders may install a P2P lending app | Real-time interest accrual |

| Attractive interest rate | |

| Gold Saving | |

| Bonds | |

| Investment Insurance | |

| Verified Credit History/Rating of borrowers |

The threshold factors and app activity together determine retention rate for P2P Lending apps while value offerings primarily drive acquisition

We collectively call them the threshold list of items. They often manifest when P2P business models are translated into the app. Most of the time, these come off as bottlenecks that prevent lenders and borrowers from fully experiencing the app’s value. After listening to many P2P app entrepreneurs it becomes apparent that:

Numerous apps silently succumb at the threshold level due to an inability to analyze the massive loads of data points from hundreds of thousands, or even millions of customers, a P2P lending app can potentially attract. It is simply not scalable.

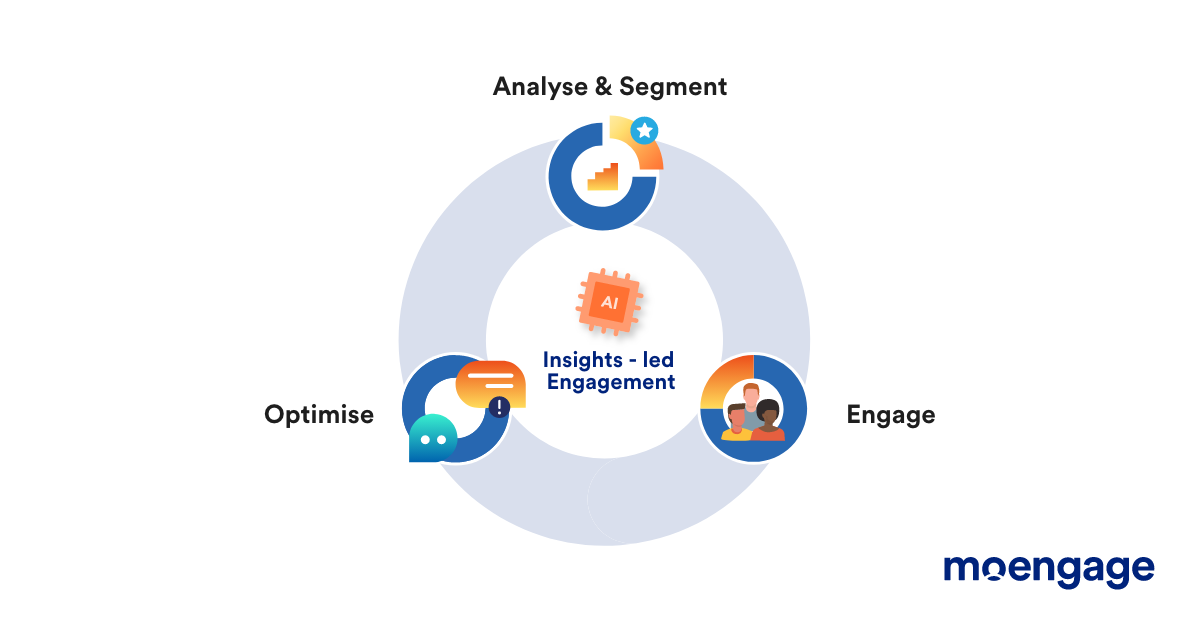

The only way to scale and make sense of such enormous data points is to employ an insights-led engagement strategy. It is a three step approach that include segmenting customers behaviorally and engage them across channels, test assumptions about the best channel(s) and message, and finally augment this behemoth of data using an AI to identify and optimize the best set of actions.

This is precisely why onboarding remains a massive game-changer for the success of P2P apps. An effective onboarding borne out of insights can reveal the broken pieces within the onboarding process and can potentially shorten the learning curve to drive a quicker app adoption.

P2P apps like MyConstant from mature markets testify to that fact. A lot of customer reviews for MyConstant revolve around a fantastic app experience that reflects a satisfied bunch of customers who are well-versed with the app features.

How do P2P Lending Apps Solve Retention Bottlenecks?

The threshold list of items is where you find the major retention bottlenecks for P2P lending apps. As mentioned, you need an insights-led approach to understand what’s going on and quickly expedite the solution. Here’s a list of three actions items:

Nail the Onboarding Process: An excellent onboarding process for a P2P app is necessary to educate your customers. They should be able to sign up quickly, be able to verify their documents, and start lending as soon as possible. On the borrower side, they must be educated rapidly on lending and withdrawal rules that potentially affect the usage patterns of features and retention in the long run.

The first step in the right direction is to understand the preferred user path of your customers at scale. Correlate the findings and point out the reasons for customer inactivity and churn. Follow up with Push Amplification™ that motivates customers to take action and transact.

Use Funnels and Cohorts to Cross the Threshold: Attribution analysis often reveals multiple paths to the desired goals you’ve set for your audience. However, some of them are special and earn you the most number of sign-ups. To quantify them and test your assumptions, you need funnels and cohorts.

While funnels can help you reinforce or reject your assumptions about customer flow, cohorts, on the other hand, give insights into how multiple customer groups are behaving. You can then look for the underlying reasons for their drop-off (if any).

Combined with user paths, funnels and cohorts can help you craft a smooth onboarding experience and let your customers go beyond the threshold factors mentioned above.

Behavioral Segmentation to Drive Recurring Usage: Once your onboarding is sorted and your best conversion paths optimized, it is time to drive recurring usage within the app.

Go for behavioral segmentation of your active customer base using RFM analysis. RFM stands for recency, frequency, and monetary, which are three variables used to behaviorally segment your customers. RFM analysis gives multiple subsets of customers you can engage with the right RFM engagement strategies.

Conclusion

P2P lending apps brings forth many opportunities for lenders and borrowers. But at the same time the challenges around building a momentum for app adoption along with driving recurring usage can be overwhelming. However, with the help of an insights-led engagement approach, you can build a great onboarding experience and keep building the right features for customers to experience the value sooner.

P2P lending apps have emerged as a widespread mode of lending in Indonesia. Their ability to generate income and support MSMEs while bringing the underbanked into the ecosystem is truly useful and inspiring.

Further Reading

RFM Segmentation: A Deeper Path to Personalization

State of Mobile Finance in 2021

Data Story: Fynd Finds 129% Increase in Retention Using Predictive Segmentation